ARFS - user defined cross validation scheme - Time series applicaition#

You can pass your own cross validation scheme to GrootCV. It might be useful for time series applications.

[3]:

import numpy as np

import matplotlib.pyplot as plt

from sklearn.datasets import fetch_openml

from sklearn.ensemble import HistGradientBoostingRegressor

from sklearn.model_selection import cross_validate

from sklearn.model_selection import TimeSeriesSplit

from arfs.benchmark import highlight_tick

from arfs.feature_selection.allrelevant import GrootCV

bike_sharing = fetch_openml("Bike_Sharing_Demand", version=2, as_frame=True)

df = bike_sharing.frame

y = df["count"] #/ df["count"].max()

X = df.drop("count", axis="columns")

X["weather"] = (

X["weather"]

.astype(object)

.replace(to_replace="heavy_rain", value="rain")

.astype("category")

)

[4]:

import arfs

print(f"Ran with numpy {np.__version__} and ARFS {arfs.__version__}")

Ran with numpy 1.26.4 and ARFS 3.0.0

[5]:

X.head()

[5]:

| season | year | month | hour | holiday | weekday | workingday | weather | temp | feel_temp | humidity | windspeed | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | spring | 0 | 1 | 0 | False | 6 | False | clear | 9.84 | 14.395 | 0.81 | 0.0 |

| 1 | spring | 0 | 1 | 1 | False | 6 | False | clear | 9.02 | 13.635 | 0.80 | 0.0 |

| 2 | spring | 0 | 1 | 2 | False | 6 | False | clear | 9.02 | 13.635 | 0.80 | 0.0 |

| 3 | spring | 0 | 1 | 3 | False | 6 | False | clear | 9.84 | 14.395 | 0.75 | 0.0 |

| 4 | spring | 0 | 1 | 4 | False | 6 | False | clear | 9.84 | 14.395 | 0.75 | 0.0 |

[6]:

X["random_num"] = np.random.uniform(0,1,size=len(X))

[7]:

ts_cv = TimeSeriesSplit(

n_splits=5,

gap=48,

max_train_size=10000,

test_size=1000,

)

[8]:

gbrt = HistGradientBoostingRegressor(categorical_features="from_dtype", random_state=42, loss="poisson")

categorical_columns = X.columns[X.dtypes == "category"]

print("Categorical features:", categorical_columns.tolist())

Categorical features: ['season', 'holiday', 'workingday', 'weather']

[9]:

def evaluate(model, X, y, cv, model_prop=None, model_step=None):

cv_results = cross_validate(

model,

X,

y,

cv=cv,

scoring=["neg_mean_absolute_error", "neg_root_mean_squared_error"],

return_estimator=model_prop is not None,

)

if model_prop is not None:

if model_step is not None:

values = [

getattr(m[model_step], model_prop) for m in cv_results["estimator"]

]

else:

values = [getattr(m, model_prop) for m in cv_results["estimator"]]

print(f"Mean model.{model_prop} = {np.mean(values)}")

mae = -cv_results["test_neg_mean_absolute_error"]

rmse = -cv_results["test_neg_root_mean_squared_error"]

print(

f"Mean Absolute Error: {mae.mean():.3f} +/- {mae.std():.3f}\n"

f"Root Mean Squared Error: {rmse.mean():.3f} +/- {rmse.std():.3f}"

)

evaluate(gbrt, X, y, cv=ts_cv, model_prop="n_iter_")

Mean model.n_iter_ = 100.0

Mean Absolute Error: 42.744 +/- 1.721

Root Mean Squared Error: 67.084 +/- 3.941

[10]:

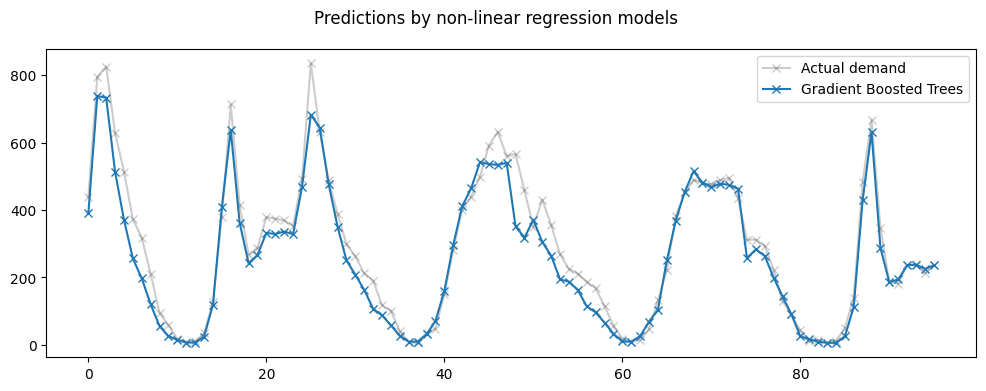

all_splits = list(ts_cv.split(X, y))

train_0, test_0 = all_splits[0]

gbrt.fit(X.iloc[train_0], y.iloc[train_0])

gbrt_predictions = gbrt.predict(X.iloc[test_0])

last_hours = slice(-96, None)

fig, ax = plt.subplots(figsize=(12, 4))

fig.suptitle("Predictions by non-linear regression models")

ax.plot(

y.iloc[test_0].values[last_hours],

"x-",

alpha=0.2,

label="Actual demand",

color="black",

)

ax.plot(

gbrt_predictions[last_hours],

"x-",

label="Gradient Boosted Trees",

)

_ = ax.legend()

[11]:

feat_selector = GrootCV(

objective="poisson",

cutoff=1,

n_folds=5,

folds=ts_cv,

n_iter=5,

silent=True,

fastshap=False,

n_jobs=0,

)

feat_selector.fit(X, y, sample_weight=None)

print(f"The selected features: {feat_selector.get_feature_names_out()}")

print(f"The agnostic ranking: {feat_selector.ranking_}")

print(f"The naive ranking: {feat_selector.ranking_absolutes_}")

fig = feat_selector.plot_importance(n_feat_per_inch=5)

# highlight synthetic random variable

fig = highlight_tick(figure=fig, str_match="random")

fig = highlight_tick(figure=fig, str_match="genuine", color="green")

plt.show()

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[220] training's poisson: -829.875 valid_1's poisson: -1353.86

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[151] training's poisson: -893.774 valid_1's poisson: -1404.89

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[231] training's poisson: -944.527 valid_1's poisson: -1516.04

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[198] training's poisson: -1010.91 valid_1's poisson: -1264.35

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[175] training's poisson: -1056.5 valid_1's poisson: -771.641

The selected features: ['season' 'year' 'month' 'hour' 'weekday' 'workingday' 'weather' 'temp'

'feel_temp' 'humidity' 'windspeed']

The agnostic ranking: [2 2 2 2 1 2 2 2 2 2 2 2 1]

The naive ranking: ['ShadowVar13', 'ShadowVar10', 'ShadowVar11', 'ShadowVar9', 'ShadowVar4', 'ShadowVar6', 'ShadowVar12', 'ShadowVar3', 'ShadowVar1', 'ShadowVar8', 'ShadowVar7', 'ShadowVar2', 'ShadowVar5']

[12]:

X_fs = X.drop(columns=["random_num", "holiday"])

all_splits = list(ts_cv.split(X_fs, y))

train_0, test_0 = all_splits[0]

gbrt.fit(X.iloc[train_0], y.iloc[train_0])

gbrt_predictions = gbrt.predict(X.iloc[test_0])

last_hours = slice(-96, None)

fig, ax = plt.subplots(figsize=(12, 4))

fig.suptitle("Predictions by non-linear regression models")

ax.plot(

y.iloc[test_0].values[last_hours],

"x-",

alpha=0.2,

label="Actual demand",

color="black",

)

ax.plot(

gbrt_predictions[last_hours],

"x-",

label="Gradient Boosted Trees",

)

_ = ax.legend()

[13]:

evaluate(gbrt, X_fs, y, cv=ts_cv, model_prop="n_iter_")

Mean model.n_iter_ = 100.0

Mean Absolute Error: 41.277 +/- 2.951

Root Mean Squared Error: 64.586 +/- 5.453

[ ]: